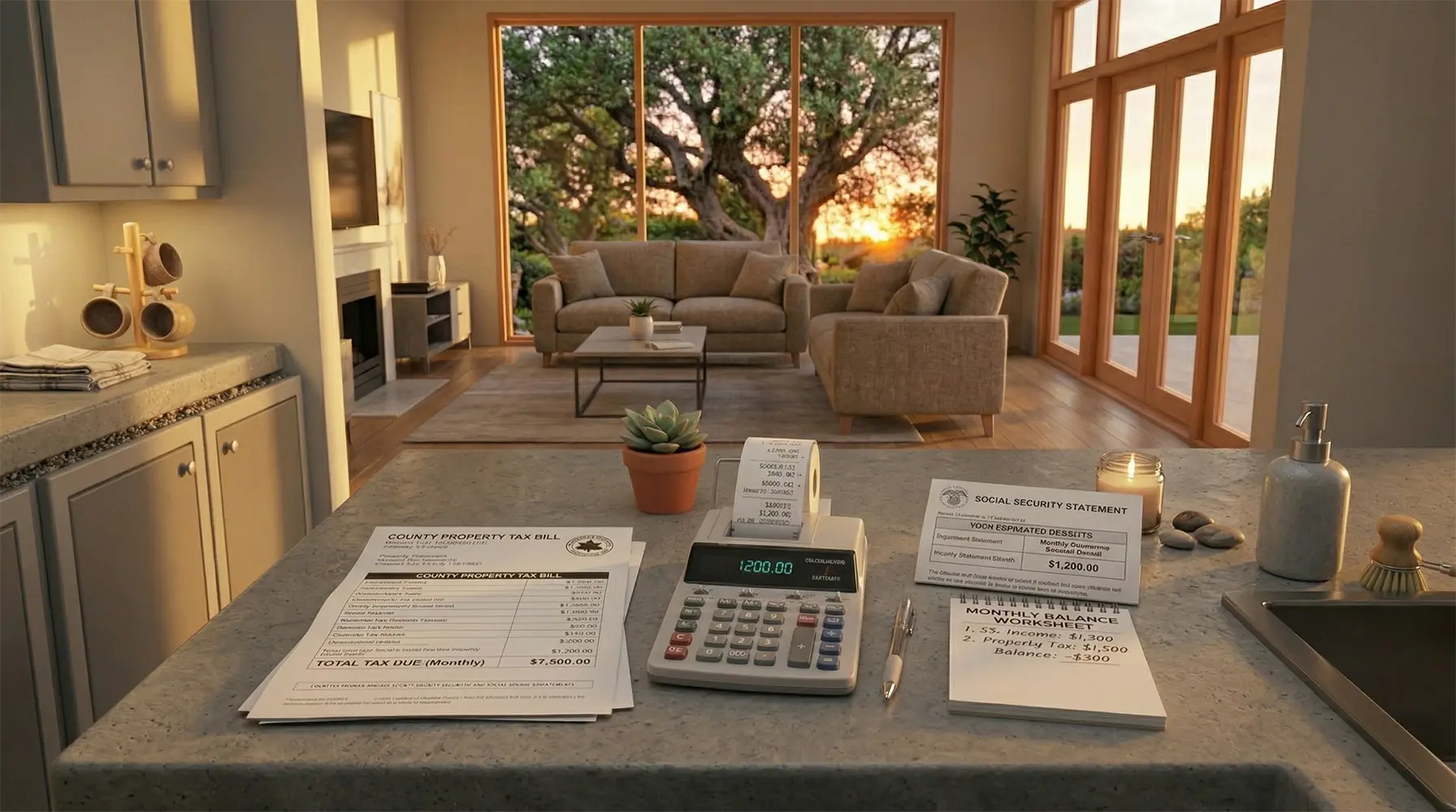

You are sixty-eight. You bought the house in 1994 for a number that now sounds like a joke. The mortgage is gone. Your Social Security check, post-Medicare deduction, lands around two thousand dollars a month. Your property tax bill just arrived, and the number on it is eleven thousand dollars — a sixty-four percent jump over five years, because your county reassessed and the levy went up.

You do not have eleven thousand dollars sitting in a savings account. You have a house worth roughly seven hundred thousand, about four hundred in an IRA, and the Social Security check. Your kids live in a different state and have their own mortgage. Your late spouse used to handle the tax bill. Now you handle it, and the math has stopped working.

This is not a hypothetical. The Census Bureau's 2024 data on median property tax burden shows effective property tax rates have climbed in every major metro, and the effect on fixed-income retirees has been particularly brutal in states without senior tax freezes. You are not doing anything wrong. The system is doing something to you.

Every retiree we have talked to has walked through the same four options, in roughly the same order. Here they are.

The advice every personal finance columnist gives. Sell the $700K house, buy a $400K condo, bank the difference. Problem solved.

The problem is that in most markets the $400K condo does not exist anymore — not in your neighborhood, not in one you would want to live in, and not with the HOA fees that eat thirty percent of the savings. The 2025 NAR data on downsizing moves shows the median retiree who "downsized" in the last three years ended up with less cash in hand than expected after moving costs, closing costs, capital gains tax on the portion of gains above the exclusion, and the upgrade cycle on the new smaller place.

Downsizing is a real option. It is not the easy option the columnists describe.

A Home Equity Conversion Mortgage, insured by HUD. You borrow against the equity, make no monthly payments, and the loan gets repaid when you die or move out.

This one has its own failure modes. The origination costs are high — often two to six percent of the home's value, front-loaded. The interest compounds. The heirs inherit a house with a large loan against it, and if they want to keep it, they have to pay off the full balance within a defined window. For a single retiree with no heirs and no emotional attachment, the HECM can be rational. For a retiree with children who expect to inherit, it often creates a conversation nobody wanted to have. The CFPB's reverse mortgage explainer covers this fairly.

The question you have to answer honestly

Do you want the house to go to your kids, or do you want the equity to go to you? The two are not the same goal, and almost nobody admits out loud that they have to pick.

A line of credit secured by the house. You keep the property, draw cash when you need it, and make monthly payments.

For retirees, the big catch is qualification. Most banks use a debt-to-income ratio that treats Social Security and pension income as what it is — fixed — but also applies a conservative loan-to-value cap. A retiree with $520K of equity and a $24K annual Social Security income will qualify for a HELOC of perhaps $100K, maybe less, at a floating rate around nine percent (as of early 2026). The monthly interest on a fully drawn $100K balance at that rate is roughly $770 — thirty-eight percent of your SS check, before you touch principal.

That math works for a retiree with a pension or a big IRA withdrawal strategy. It does not work for a retiree whose income is Social Security only. There is a longer piece on what to do when refinancing is off the table that covers this scenario in more detail.

Sell the house to a buyer, sign a lease, keep the keys. Walk away with the equity, pay rent going forward.

This is the option most retirees have never heard of, and the one most financial columnists do not mention because the product is too new to have a consensus take. The appeal is that it solves the property tax problem directly — you do not pay property tax on a house you do not own. The rent you pay is the rent, period, and it is usually lower than the all-in cost of owning the house once you add taxes, insurance, and maintenance reserves.

The drawback is that you convert a bounded problem (eleven thousand dollars in property tax) into a different bounded problem (a rent payment that escalates annually, on a lease with a defined end). The numbers only work if the rent is manageable, the lease is long enough, and the escalator is capped.

Let us put real numbers against each option for a retiree who fits the profile at the top of this piece.

Starting point: $700K home, $0 mortgage, $24K Social Security, $400K IRA, $11K property tax bill.

Downsize: Cash on day one — roughly $230K net after all fees. Year-5 housing cost — roughly $30K (HOA plus tax on condo). Equity at year 5 — roughly $230K plus 2% appreciation. You live in a condo, not your original home.

HECM reverse mortgage: Cash on day one — up to roughly $250K as a credit line. Year-5 housing cost — $0 direct, but interest compounds. Equity at year 5 — declining, a function of how much you draw. You still own the house, with a lien.

HELOC: Cash on day one — up to $100K as a credit line. Year-5 housing cost — roughly $46K in interest over 5 years at 9.25%. Equity at year 5 — roughly $520K still in the home. You still own it, with a second lien.

Sale-leaseback: Cash on day one — roughly $560K net after discount and closing. Year-5 housing cost — roughly $198K in rent with a 3.5% annual escalator. Equity at year 5 — $0. You do not own the house.

Every row is defensible. Not every row is rational for every retiree.

The downsize row wins on simplicity and loses on "do I want to leave this neighborhood." The HECM row wins on monthly cash flow and loses on inheritance. The HELOC row wins on total cost and loses on qualification and monthly burden. The sale-leaseback row wins on immediate cash and loses on permanence.

— The numbers, done honestly

This is the section nobody writes. We are writing it.

If you have adult children, they have an opinion about what happens to the house. That opinion is usually some combination of "we want you to be comfortable" and "we assumed we would inherit it." Those two things are not always in conflict, but they often are.

If you choose the HELOC path, the house still goes to them, but smaller. If you choose the downsize path, the condo goes to them, much smaller. If you choose the HECM path, the house is theirs but with a balance they have to pay off. If you choose the sale-leaseback path, there is no house to leave them, but there may be more cash in your estate when you die than any of the other paths produce.

The honest conversation is: "I am going to pick the option that lets me stay in the neighborhood and not worry about money for the rest of my life. I am telling you now which option that is so we do not have to have a fight about it later." Have this conversation before you sign anything. The longer piece on tapping equity without moving includes a script for this conversation that has been useful.

Our rule of thumb, pressure-tested against maybe fifty retiree conversations:

The sale-leaseback is the right call when (a) a HELOC is unavailable or unaffordable, (b) downsizing would force a move you are not emotionally ready for, (c) the HECM's inheritance implications would create a family fight worse than the tax bill, and (d) the specific lease you have been offered has a multi-year term with a rent escalator capped at four percent or below.

All four conditions have to be true, not just one. If the escalator is eight percent, walk away. If the lease is one year, walk away. If the buyer is a single-LLC with no institutional backing, walk away. The longer piece on what to look for in a leaseback operator covers the buyer-side due diligence in detail, and it is the part of the process most retirees skip because it is boring.

We are not going to tell you this is easy, or that there is a right answer, or that the first company you talk to is the right one. We are going to tell you that the eleven-thousand-dollar property tax bill is not a personal failure and that there are four legitimate paths forward. Pick the one that loses you the least of what you care about most.

And if you are reading this piece because your parent is in this situation and you are trying to help them from another state — send them this article, talk to them about the four paths, and then help them get a second opinion from someone whose fee does not depend on which path they pick. That is the whole playbook. Everything else is detail.